business

Khalti - IME Pay Merge, Nepal Rastra Bank Shuts Two Wallets

by Khatapana

Jun 20, 2025 - 10 min read

Share

Khalti and IME Pay just merged to create Nepal’s biggest wallet, while NRB shut down two rivals. But what’s really happening behind the scenes? Read more to uncover the full story.

Some weeks pass by quietly. This one didn’t.

In the span of just a few days, Nepal’s digital payment world saw two major headlines. Opposite in tone, but deeply connected in meaning.

First, on June 19, 2025, Nepal Rastra Bank (NRB) granted final approval for something that’s never happened before in the country’s fintech history: a merger between two major digital wallets: Khalti and IME Pay. The consolidation in the online payment space has started. This move officially created Nepal’s largest digital wallet, with over 5 million verified users under a new unified entity named IME Khalti Limited.

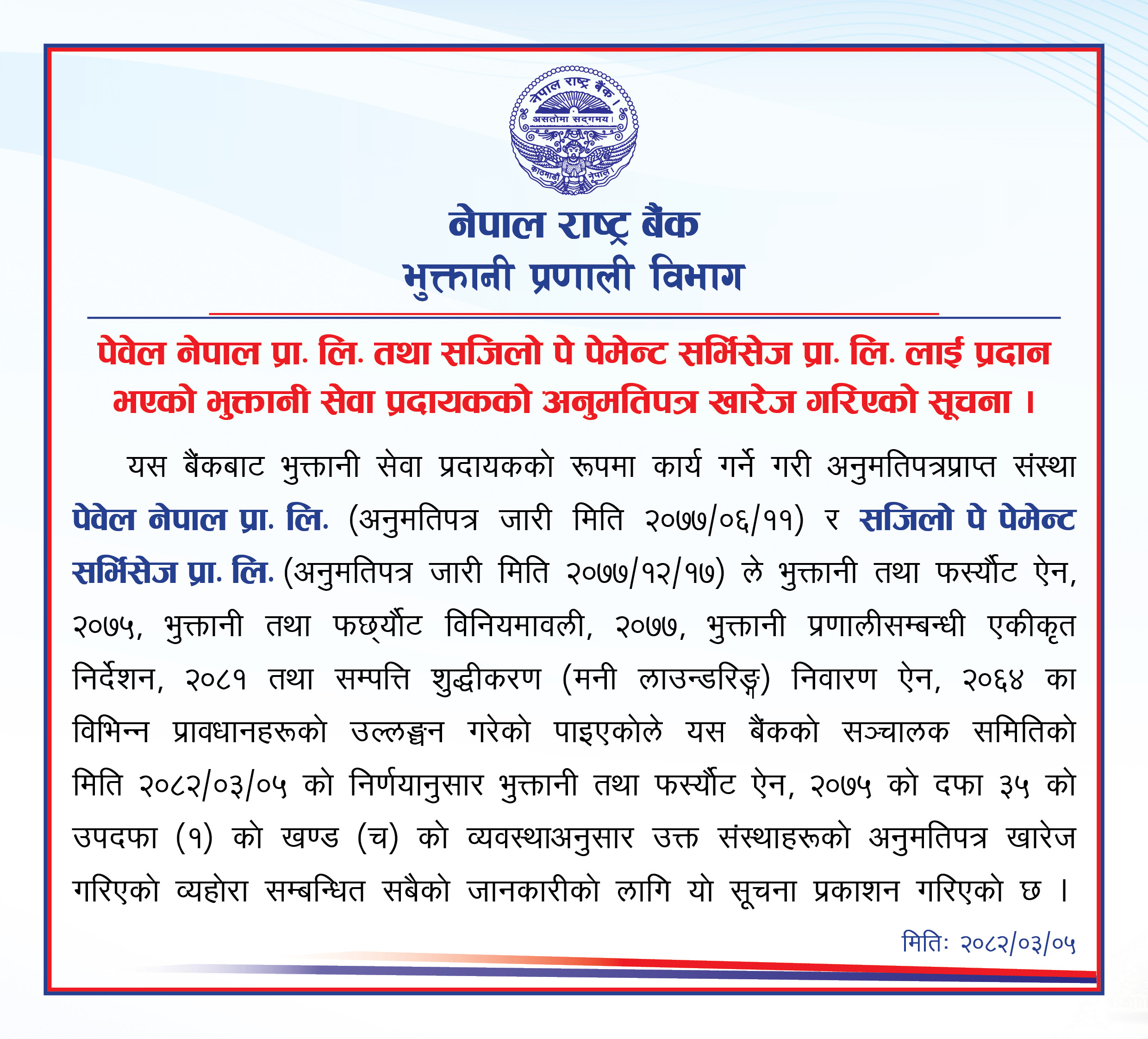

At the same time, an entirely different story was unfolding. The Central Investigation Bureau (CIB) revealed a massive underground operation involving Paywell and Sajilo Pay, two smaller PSPs that facilitated over Rs. 123 billion in illegal hundi transactions and gold smuggling activities. The fallout? NRB revoked their licenses, and several key executives were arrested.

Two major digital wallets joined forces. Two others were kicked out of the game entirely. And this ideally brings down the total number of payment service providers (PSPs), the legal term for these digital wallets, to just 23.

It’s a defining moment, not just for those four companies, but for Nepal’s entire digital payment landscape. These back-to-back developments mark a new phase in NRB’s regulatory posture: strategic on growth, but completely uncompromising on compliance. In a sector that processes over Rs. 6.2 trillion annually, the message couldn’t be clearer:

If you're building trust, scale, and transparency, like Khalti and IME Pay, you’ll find the space to grow. But if you’re operating in the shadows, your days are numbered.

1. From Rivalry to Unity: The IME Pay–Khalti Merger

If you’ve made a digital payment in Nepal recently, chances are it was through Khalti or IME Pay. These two platforms have been among the most recognizable names in the market, popular for everything from utility payments to reward offers.

But instead of continuing the rivalry, they’ve decided to team up.

The merger understanding was first signed on February 16, 2025, and received final approval from Nepal Rastra Bank on June 18. It officially forms IME Khalti Limited, a new unified entity that retains the Khalti app and brand name. This wasn’t just a branding decision, it was strategic. With over 5 million downloads on the Google Play Store, Khalti enjoys stronger public recognition, giving the combined company a head start in retaining user loyalty.

1.1 Combining Strengths to Challenge the Leader

This isn’t just about symbolism, there’s serious scale behind this move.

- The new entity combines IME Pay’s Rs. 300 million in paid-up capital with Khalti’s massive user base.

- With more than 5 million verified users, IME Khalti Limited becomes Nepal’s largest digital wallet by user base after eSewa, which still leads the market with over 10 million users and about 75% of transaction market share.

This merger brings together the best of both platforms:

- IME Pay’s strengths in international remittance and financial backing from the IME Group

- Khalti’s dominance in app usability, reach, and day-to-day utility services

Together, they form the first real challenger to eSewa’s long-standing dominance.

1.2 A Seamless Three-Month Transition Plan

Mergers in fintech can get messy, but this one’s being rolled out with care.

Over a three-month transition period, both Khalti and IME Pay apps will remain active. During this time:

- Users can merge accounts with a single tap

- IME Pay users will be migrated to Khalti, but only after they opt in

- All balances, reward points, and account history will carry over, critical in a market where many users choose wallets based on cashback, points, and ease

This careful rollout signals thoughtful planning aimed at minimizing disruption while maximizing user retention.

1.3 A Roadmap That Goes Beyond Payments

This merger isn’t just about competing on QR codes.

The newly formed IME Khalti Limited is aiming for something bigger: becoming a full-fledged digital financial platform. That includes:

- Remittance services built on IME Pay’s backbone

- Virtual banking capabilities

- Visa card issuance

- Access to credit through the app

It’s all part of a larger mission to support financial inclusion, especially in rural areas where traditional banking services remain limited or nonexistent.

The timing couldn’t be better. Nepal’s digital payment market is projected to grow to USD 4.3 billion by the end of 2025, with a 30% annual growth rate through 2029. With this merger, Khalti and IME Pay aren’t just keeping up, they’re positioning themselves to lead.

2. What This Means for the Fintech Landscape

2.1 The Age of Consolidation Is Here

Nepal’s digital wallet scene has long been buzzing with activity. More than two dozen providers, all trying to carve out their share of the market. But here’s the reality: when everyone’s offering the same thing, the market gets cluttered, not competitive.

That’s where the Khalti–IME Pay merger comes in. It’s not just a power move, it’s a turning point.

Nepal Rastra Bank’s own Payment and Settlement Bylaws 2077 were updated to encourage exactly this kind of merger and acquisition activity. The goal? To focus on quality of service over the sheer number of providers. Out of all the PSPs that once held licenses, only 23 remain active. The writing’s on the wall: scale matters, and consolidation is no longer optional. It's part of the central bank’s long-term vision for the sector.

2.2 Trust Is the New Currency

There’s a clear pattern emerging: if you follow the rules, show transparency, and serve real users; not just numbers on a dashboard, NRB will back you.

That’s exactly what we’re seeing with Khalti and IME Pay. The merger approval didn’t just come because they’re big. It came because both platforms had proven records in KYC compliance, regulated operations, and actual contribution to financial inclusion. That’s the trust-regulation feedback loop in action and it’s now the norm in Nepal’s fintech journey.

Compare that with what happened to Paywell and Sajilo Pay (more on that in a second), and the contrast is crystal clear. In a market that processes over Rs. 6.2 trillion annually, integrity is infrastructure.

2.3 A Timely Boost from Infrastructure Upgrades

This isn’t happening in isolation either.

Nepal’s broader payments ecosystem is improving fast. The merger aligns perfectly with recent rollouts like:

- QR interoperability between NEPALPAY QR and SMARTQR, now used by over 230,000 merchants

- Cross-border UPI integration with India, launched in March 2024, which processed over Rs. 250 million in transactions in just its first year

With their combined tech and user base, Khalti and IME Pay are now uniquely positioned to accelerate QR unification and push for standardized reward systems across platforms. It’s not just a merger, it’s a real shot at creating a seamless, national payment experience.

Did you know that Nepal already accepts foreign QR payments via local digital wallets like eSewa & Khalti? Discover how this could boost tourism, SMEs & digital payments across the country.

3. The Dark Side: When Fintech Crosses the Line

While Khalti and IME Pay were building momentum, Paywell and Sajilo Pay were heading in the opposite direction, and fast.

This wasn’t just non-compliance. This was organized financial crime.

According to Nepal’s Central Investigation Bureau, the two platforms facilitated nearly Rs. 123 billion in questionable transactions between April 2023 and June 2024. These weren’t regular payment flows, they were set up to bypass the banking system and enable illegal hundi operations, gold smuggling, and unrecorded cash transactions.

- Paywell alone processed over Rs. 86 billion, with more than Rs. 61 billion flowing through shady voucher deposits.

- Sajilo Pay handled Rs. 36.94 billion, with Rs. 19 billion using the same loophole: unregulated, unverifiable uploads that skipped the KYC process entirely.

3.1 The Laws They Broke

The violations stacked up fast:

- Breach of the Payment and Settlement Act 2075

- Breach of the Money Laundering Prevention Act 2064

- Multiple infractions under Unified Directive 2081

But that’s just the beginning.

They didn’t just let bad actors use their platforms. They actively submitted false data to NRB on daily and monthly transaction volumes, deliberately misreporting activities to hide what was going on. Some merchant agents were even using the platforms like ATM counters, taking in and handing out cash without any official records.

This wasn’t negligence. It was a full-blown scheme.

3.2 Global Reach, Criminal Depth

The scandal didn’t stop at Nepal’s borders.

Investigators found links to Australia, the UAE, and South Korea, where remittance flows were being quietly rerouted and laundered through the two apps. Meanwhile, proceeds from gold smuggling operations were deposited straight into users’ accounts back home, creating a loop of illegal financial flows masked as fintech.

The operation went all the way to the top. Eight individuals, including senior executives and board members, were arrested. The platforms weren’t just exploited by bad actors. They were being run by them.

3.3 A Tale of Two Paths

If the Khalti–IME Pay story is about vision, trust, and strategic growth, this is the cautionary tale that shows the cost of cutting corners. In a rapidly evolving ecosystem, NRB is no longer tolerating half-measures or blind spots. It’s raising the bar, and expecting everyone to meet it.

Because in the end, it’s not about who launched first. It’s about who plays fair, builds trust, and stays in the game.

4. Why Is Nepal Rastra Bank Cracking Down Now?

When Nepal Rastra Bank (NRB) approved the country’s biggest digital wallet merger and cancelled two PSP licenses in the same week, it wasn’t just coincidence. It was coordination. And more importantly, it was strategy.

For years, Nepal’s digital finance space had been sprinting ahead. Apps were launching, user numbers were climbing, and everyone was celebrating growth. But beneath the surface, compliance was struggling to keep pace. Some platforms played by the rules. Others exploited the system. Some, like Paywell and Sajilo Pay, were eventually exposed for using their licenses as shields for illegal activity.

That’s when NRB drew a hard line.

4.1 Global Pressure: FATF Grey List and the Race Against Time

In February 2025, Nepal landed back on the Financial Action Task Force (FATF) grey list. The reason? Weak enforcement of anti-money laundering (AML) rules and lack of control over high-risk sectors like fintech.

NRB now has a two-year window to get things in order, or risk a potential blacklisting, which would severely restrict Nepal’s ability to engage with global financial markets. That’s why enforcement is no longer optional. It’s urgent.

And the crackdown on non-compliant PSPs? That’s step one.

4.2 New Rules, New Tools: The Rise of RegTech in Nepal

NRB isn’t just rewriting rules, it’s upgrading the entire playbook.

A new directive (Directive No. 5) now mandates all financial institutions, including PSPs, to:

- Conduct stress tests

- Flag high-risk clients like politically exposed persons (PEPs) and HNWIs

- Regularly report to NRB on AML/CFT risk

At the same time, the Financial Intelligence Unit is using AI and big data analytics to track suspicious activity in real time. As a result, suspicious transaction reports (STRs) are on the rise, and NRB is spotting violations that would have flown under the radar just a few years ago.

So yes, the crackdown is tough, but now it’s also tech-powered.

4.3 Not Anti-Fintech, Just Anti-Fraud

Here’s the nuance: NRB isn’t against fintech innovation. In fact, it’s pushing for it.

Policies like cross-border IT investment, QR code interoperability, and UPI integration with India show just how serious the regulator is about building a modern payment infrastructure. But the message is clear: only serious players will be allowed to grow.

You can’t just slap together an app, skip compliance, and expect to survive. You’ve got to earn it.

5. A Market at the Crossroads?

Right now, Nepal’s digital payments ecosystem is at a critical juncture.

On one side, you’ve got platforms like Khalti and IME Pay, merging resources, expanding services, and aligning with national goals like rural financial inclusion and cashless growth. Their roadmap includes virtual banking, in-app credit, and remittance tools that reach beyond the city.

On the other side, you’ve got what Paywell and Sajilo Pay exposed: a darker path where licenses are misused, compliance is performative, and the system is treated like a loophole.

NRB’s latest moves make it very clear which path leads to survival, and which leads to shutdown.

5.1 Real Enforcement, Real Consequences

Let’s not forget: this isn’t just policy. It’s enforcement.

The Paywell–Sajilo Pay case triggered immediate license cancellations and arrests. And the new rules go even further:

- PSPs must eliminate existing agent networks within three months

- All field representatives must now be board-approved and audited directly by NRB

- Daily and monthly limits (Rs. 5,000/day and Rs. 25,000/month) now apply to transactions via these representatives to cap exposure to cash-based abuse

This level of micro-regulation reflects just how seriously NRB is taking market hygiene.

5.2 A Growing Market, with Room for the Right Players

Despite the recent cleanups, this isn’t a shrinking market, it’s an expanding one.

- Mobile banking users grew from 6.48 million in 2020 to 24.65 million by mid-2024, a 280% surge

- QR code merchants rose from 282,000 in 2021 to over 2.34 million by Jan 2024

- And yet, only 5% of Nepal’s economy is currently digitized, meaning the opportunity is massive for those who can scale responsibly

For users, this all translates into a more trustworthy ecosystem. For serious operators, it’s a greenlight to grow. And for NRB? It’s proof that strong oversight and smart innovation can exist in the same sentence.

6. What to Expect Next

With the successful merger of Khalti and IME Pay, don’t be surprised if more wallets start joining forces. Out of the 23 remaining PSPs in Nepal, many are already feeling the pressure, tightening compliance rules, rising costs, and stricter oversight mean only those with real scale can survive.

And the bar isn’t theoretical. NRB has set actual business milestones: to keep their license, PSPs must reach at least 300,000 active customers and log 600,000 monthly transactions. For smaller players, that’s a tall order. Some will chase merger opportunities. Others may quietly disappear.

We’ve officially entered the era of survival by scale and compliance.

6.1 Compliance Is No Longer a Checkbox, It’s a Culture

Every licensed PSP now has new obligations:

- Submit quarterly digital transaction reports

- File biannual compliance summaries

- Obtain board-level approval for field representatives

- Completely phase out legacy agent networks, which were often loopholes for cash-based abuse

These steps aren’t just red tape, they’re designed to eliminate shadow operations like those exposed in the Paywell–Sajilo Pay scandal. And yes, the focus is sharpest on wallets operating near border zones or serving high-risk user segments.

6.2 Trust Through Technology

The good news? Platforms that invest in transparency, compliance infrastructure, and seamless UX won’t just survive, they’ll lead.

Khalti and IME Pay have already set the tone. Their vision for a unified platform that offers virtual banking, credit access, remittance, and secure payments reflects what the new fintech standard looks like. And in a market where only 5% of the economy is currently digitalized, the room for compliant, user-friendly growth is massive.

So what should users expect?

- Fewer but stronger wallets

- Apps that actually work across platforms

- Reward systems that make sense

- Faster, safer payments with less friction

Behind the scenes, more real-time monitoring, smarter fraud detection, and stricter KYC rules will make sure digital convenience doesn’t come at the cost of financial security.

Final Thoughts

This wasn’t just an eventful week. It was a turning point.

On one end, the Khalti–IME Pay merger showed what’s possible when vision meets structure. It proved that with the right mix of scale, compliance, and user focus, Nepal can create homegrown fintech leaders capable of driving meaningful financial inclusion.

On the other end, the Paywell–Sajilo Pay takedown reminded everyone what happens when that responsibility is ignored.

Together, they lay down a clear blueprint for the future.

Consolidation isn’t just likely, it’s necessary.

Compliance isn’t a technicality, it’s the baseline.

Growth isn’t just about getting bigger, it’s about getting better.

As Nepal works to exit the FATF grey list by 2027, every fintech player now has a choice: evolve with the ecosystem or get left behind. The companies that embrace real governance, clean data practices, and regulatory alignment won’t just survive, they’ll shape what comes next.

With the digital payment market expected to reach USD 11.14 billion by 2029, the opportunity is enormous, but only for those playing the long game.

Nepal’s digital payment space isn’t just growing. It’s maturing.

And if this week is any indicator, the future will belong to the platforms that know how to grow, responsibly, sustainably, and transparently.

Additional Resources:

- eSewa & Khalti Can Now Accept Foreign QR Payments in Nepal

- How NRB’s New Directive Impacts Khalti, Mobile Banking, and Digital Nepal

- Nepal Rastra Bank Finally Lets IT Companies Go Global

- Is Nepal Electricity Authority Risking Rs. 66B in Hydropower?

Help Center

Help Center

{kind=link}